Advertisement

Central Bank Watch Overview:

- The second week of the year was all about the Federal Reserve and policymakers speaking out against early tapering or a rate hike.

- In fact, Fed Chair Jerome Powell’s comments on a Princeton University webcast suggest that the Fed will be keeping its QE in place for at least 2021, and its main rate low through 2023.

- Retail trader positioningsuggests a mixed outlook for EUR/USD, while GBP/USD has a bullish bias.

Central Banks Mostly Quiet…

2021 has produced little by way of volatility induced by central banks. A few items have appeared here or there without a sustained market reaction: Bank of England policymakers’ public discussions regarding negative interest rates, or European Central Bank President Christine Lagarde’s comment about “funny business” in Bitcoin and cryptocurrency markets.

For more information on central banks, please visit the DailyFX Central Bank Release Calendar.

In this edition of Central Bank Watch, we’ll review the speeches made in the past few days by the slew of Federal Reserve policymakers, including Fed Chair Powell earlier on Thursday.

Federal Reserve Tamps Down Taper Tantrum

Many of the other major central banks haven’t been in the news this year yet as they’re not anticipated to meet until later in January or not until February. Instead, all attention has been on the Federal Reserve, which had been floating trial balloons regarding a potential tapering of bond purchases later this year. Qualifying the conversation around a potential ‘taper tantrum’ has been front and center.

January 11 – Bostic (Atlanta Fed president) sees Fed rates on hold in 2021, with a potential rate hike coming in the second half of 2022. “I’m prepared to support pulling back and recalibrating a bit of our accommodation and then considering moving the policy rate…but I don’t see that happening in 2021.” Kaplan (Dallas Fed presisdent) said that a tapering discussion could take place later this year.

January 12 – Rosengren (Boston Fed president) said that “Fed will keep short-term rates low until inflation achieves 2% on a sustained basis, and continue to purchase longer-term assets until economic growth is on a stronger footing.” George (Kansas City president) said the FOMC won’t react until inflation “tips above 2%.”

January 13 – Bullard (St. Louis president) said Fed must “regain credibility” on the 2% inflation target, and that “we are not going to be preemptive in that sense, we aregoing to let inflation go over target.” Brainard (Fed governor) suggests tapering is far away: “Given my baseline outlook, I expect that the current pace of purchases will remain appropriate for quite some time.” Clarida (Fed vice chair) said that rates won’t rise until inflation stays at 2% for “a year.”

January 14 – Daly (San Francisco president) said that she’s “not at all worried that there’s this run-up in inflation around the corner that we will need to preemptive stave off.” Powell (Fed chair) said “at the end of the day the public will need to see us allow inflation to move moderately above 2% for a time before the new framework will be seen as fully credible.” When asked about the timing of a rate hike, he responded with “no time soon.”

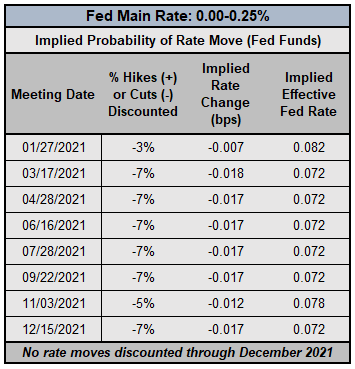

Federal Reserve Interest Rate Expectations (January 14, 2021) (Table 1)

Accordingly, with Powell at the helm, the course that he has thus far charted will not be deterred or altered: interest rates will remain low through 2023, as the Fed has indicated after each of the past three recent FOMC meetings. Fed funds futures are pricing in a 93% chance of no change in Fed rates in 2021.

Recommended by Christopher Vecchio, CFA

Get Your Free USD Forecast

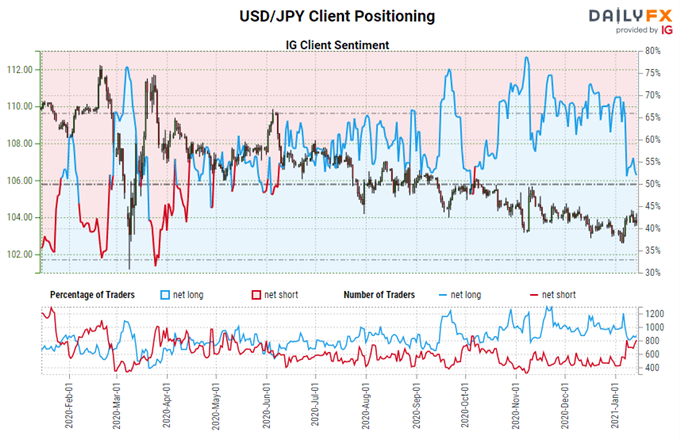

IG Client Sentiment Index: USD/JPY Rate Forecast (January 14, 2021) (Chart 1)

USD/JPY: Retail trader data shows 69.34% of traders are net-long with the ratio of traders long to short at 2.26 to 1. The number of traders net-long is 12.34% higher than yesterday and 7.25% higher from last week, while the number of traders net-short is 10.11% lower than yesterday and 0.84% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests USD/JPY prices may continue to fall.

Traders are further net-long than yesterday and last week, and the combination of current sentiment and recent changes gives us a stronger USD/JPY-bearish contrarian trading bias.

— Written by Christopher Vecchio, CFA, Senior Currency Strategist

|

|

Leave a Reply

You must be logged in to post a comment.