Dow Jones: A True Cross Section of American Industry?

If you ask a financial analyst or expert trader how to get a picture of where the global economy is currently headed, they will likely tell you to consult the Dow Jones Industrial Average. The second-oldest market index in the US, the Dow Jones today is a vital indicator of the health and direction of travel of the world’s largest and most globalized economy. But delving a little deeper, is it still an accurate cross section of the American industry of today?

- The History of the Dow Jones Industrial Average: 1884-2020

- Is the Dow Jones Still Purely Industrial?

- Dow Jones and the White House

- Does the Dow Jones Represent the US Economy?

- Dow Jones vs The World

- Conclusion

Put simply, the Dow Jones Industrial Average is a collection of the 30 largest American companies, representing $8.33 trillion in total market capitalization today, with Dow Jones stock generally among the most sought-after and heavily traded in the world.

However, the Dow Jones is more than just a ranking of the top performers in the US economy. Its performance largely (although not always) mirrors that of the American economy, and a bad day for the Dow Jones is almost invariably a bad day for the world. Understanding the Dow Jones and what makes it tick is imperative for any budding economist, analyst, trader, or investor. The myriad factors that cause the Dow Jones ticker to move up or down reflect the social, political, cultural, and technological developments that continue to shape the global economy today.

The 30 companies that make up the Dow Jones right now are all household names that are known the world over, even by those with only a passing interest in business and finance. However, does that mean that the Dow Jones is actually a fair representation of the US economy? Throughout the years, numerous criticisms have been leveled at the Dow Jones by market watchers who believe that it does not paint an accurate picture of the economy at large.

There are many arguments put forward to justify this position, with the most prominent one being that the Dow Jones, with only 30 companies represented, is much too limited compared to other US indices such as the S&P 500 or the Russell 3000. Nonetheless, the Dow Jones is still one of the most respected and heavily consulted and traded indices on the planet. Let’s take a closer look at the long and eventful history of the Dow Jones, before assessing whether it still provides a representative snapshot of the US economy in 2020.

The History of the Dow Jones Industrial Average: 1884-2020

The Dow Jones Industrial Average, is, after the Dow Jones Transportation Average, the oldest stock index in America, and one of the oldest indices of its kind in the world. It is therefore unsurprising that it has seen considerable ups and downs and plenty of drama, given that it has affected and been affected by some of the most important events in world history. As the DJIA enters its 135th year of existence, let’s take a look at some of the most noteworthy periods in its existence.

Source 1: Investopedia

Source 2: Investors

Source 3: Listen to the Music by Steve Richards

Source 4: Investopedia

Source 5: New York Times

Source 6: The Stock Market by Donna Jo Fuller

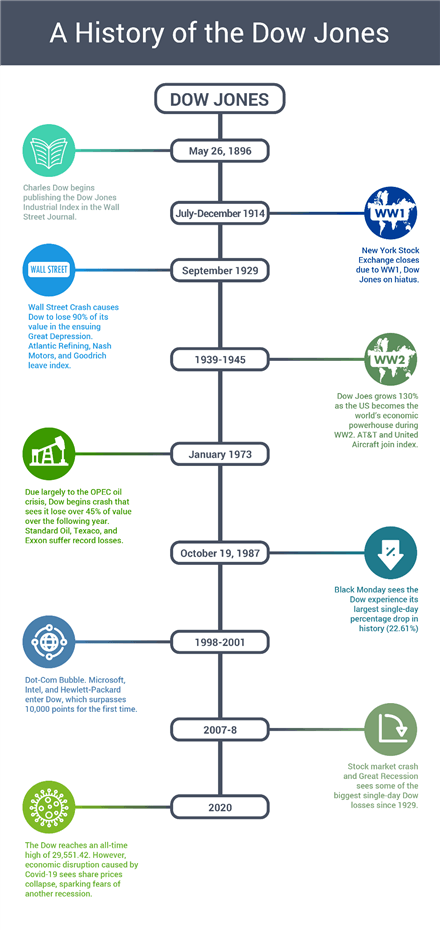

Early Years (1884-1914)

The DJIA was originally developed by Charles Dow, the journalist who founded the Wall Street Journal and pioneered a number of groundbreaking theories of market analysis that are still widely used today. The earliest conception of the index came in the form of a daily two-page bulletin attached to issues of WSJ, which would summarize the performance of 14 largely transportation-oriented companies that day. It wasn’t until 1896 that Charles Dow decided to calculate an average index of the largest industrial stocks, in the hopes that such an index would be more useful for those trying to get a comprehensive snapshot of the wider economy. The Dow Jones Industrial Average index first consisted of 12 companies that represented the crème de la crème of American industry. Although some of these companies are still going strong today, none of them have featured on the Dow Jones trading index for a while. Here is the full Dow Jones companies list of the very first components, as they appeared 124 years ago:

- American Cotton Oil Company (now a subsidiary of Unilever)

- American Sugar Refining Company (now Domino Foods Inc.)

- American Tobacco Company (defunct)

- Chicago Gas Company (now a subsidiary of Integrys Energy Group)

- General Electric (left Dow Jones in 2018)

- Laclede Gas Company (now Spire Inc.)

- North American Company (defunct)

- Tennessee Coal, Iron and Railroad Company (acquired by US Steel in 1907)

- United States Leather Company (defunct)

- United States Rubber Company (acquired by Michelin in 1990)

When the index was first published, it stood at a mere 62.76 points. Compare this to the record-high of 29,551.42 points, reached on February 12, 2020, and it is clear that the Dow Jones has come a long way since then.

While the first few years of the DJIA were relatively muted compared to later decades, it did see many of the most significant percentage point shifts in its history, owing largely to the smaller size overall. Up until the turn of the 20th century, the Dow Jones rose steadily and was virtually uninterrupted. However, this quickly changed as some of the earliest panics and bubbles in American history began to impact on the most important industrial players. 1901 saw the New York Stock Exchange’s first-ever crash, aptly dubbed the ‘Panic of 1901’. This brief but dramatic crash, which wiped 16 points off the Dow Jones in a single day, was largely driven by railroad executive E.H. Harriman competing with J.P. Morgan to acquire majority ownership of the Northern Pacific Railway. To achieve this, Harriman began furiously buying up stock in the company, which in turn caused a market distortion leading to a bubble, then a panic, then a crash that affected all companies on the Dow Jones stock market.

A more dramatic crash and the first truly major test for the DJIA came a few years later, in 1907. At this time the USA was in the midst of a recession, and the sudden collapse of a number of prominent trust companies, most notably the Knickerbocker Trust Company, sparked panic and a run on the banks that wiped as much as 50% off the value of the Dow Jones average in just a few weeks. The following decade was characterized by minor gains punctuated by short crises. The Dow Jones closed at over 100 points for the first time in 1906. However, this milestone was quickly overshadowed by the San Francisco Earthquake that same year, which impacted all of the Dow Jones companies at the time due to the widespread economic uncertainty generated by one of America’s worst-ever natural disasters. Perhaps the most significant period for the DJIA during these early decades concerns a lengthy amount of time where there was a lack of volatility on the index.

On July 30, 1914, the unthinkable happened; the New York Stock Exchange was closed outright for a period of four months, with no trading whatsoever being allowed to take place. This was the first and only time that Wall Street effectively shuttered its doors and placed the stock market on lockdown. These days, when trading is paused, it is usually done so via a breaking switch on the trading floor, and the pause only lasts for around 15 minutes, with the intention of slowing down selloffs during a panic. This unprecedented decision was taken by William Gibbs McAdoo, the US Treasury Secretary, for two reasons. The first was to reduce the chance of a sustained market crash as a result of the onset of the First World War. The second, although this is still up for debate among historians, was because it was believed that restricting trading would allow the United States to build up its gold stocks prior to the launch of the United States Federal Reserve in late 1914, ensuring that the US had enough gold to remain on par with the Gold Standard. By the time the New York Stock Exchange, and by extension the DJIA, had reopened in December 1914, much of the globe was embroiled in bloody conflict.

Boom, Bust, and Boom (1914-1960)

On the face of things, the First World War was a relatively muted time for the Dow, at least if you look at the Dow Jones historical data for that time. The index rose slowly and steadily from 1914 to 1918, with virtually zero notable booms or crashes. However, when you compare the DJIA to indices from around the world at the time, it’s clear that the situation was far from normal. In the UK, share values on the London Stock Exchange declined heavily during the war, as demand for British exports and futures dried up. Markets in Berlin and St Petersburg remained closed from 1914 right up until December 1917, meaning that listed companies saw no appreciation or decline whatsoever during this time. Meanwhile, all of the companies listed on the DJIA saw their share prices and market caps rise during what was at that point the most significant economic downturn in human history.

Following its bottom in November 1914, the Dow Jones Industrial Average doubled in price over the course of the next 12 months. The few months after that saw very little growth, but a major rally in 1916 saw strong growth, before plateauing out in the final months of the war as investors realized that the profits they had hoped would materialize from the war were much more modest than predicted. So how can this be explained? Largely this unexpected growth can be attributed to the strong position of Dow listed companies in a wartime economy. The biggest stock rises were seen in constituents such as General Electric, United States Rubber Company, and American Cotton Oil Company, which saw global demands for their products skyrocket. Since few other countries were able to muster up the manufacturing power of the US at this time, the Dow Jones was able to charge ahead while other indices around the world stalled or fell.

Following the conclusion of the war and a brief global recession as the global economy took stock, the American economy and the Dow Jones entered one of its most spectacular growth periods in history. The Roaring Twenties, as the period is now known, was a period of rapid economic expansion and prosperity during which global stock markets rapidly rose to dizzying heights, before crashing spectacularly. The euphoria of the decade is best reflected in the movements of the Dow Jones: 1920 to 1929 saw the most dramatic bull run in its history, rising from 73 to 381, a five-fold increase. At the peak of the market, the DJIA was officially expanded to include 30 companies rather than just 12, just as it does to this day. Of course, we all know what happened next.

In late September 1929, the bubble burst and the most devastating crash in American history began, emanating outwards from Wall Street and causing untold destitution over the course of the next decade. At the lowest point of the Great Depression, the Dow Jones lost almost 90% of its value, and the high reached on September 3, 1929, was not reached again until 1954. Recent newcomers to the DJIA such as Atlantic Refining, Nash Motors, and Goodrich were promptly kicked off the index as their share price collapsed, never to return.

While the 1930s were marked by stagnation and recession, the 1940s brought the biggest boost yet for the Dow Jones. At the darkest depths of the Second World War, soaring demand for American exports in Europe helped propel the Dow Jones to dizzying new heights and lay the foundations of the most prolonged period of prosperity in US history. The Dow grew 130% between 1942 and 1945, the three years that the United States was involved in the war.

During the post-war boom in the 1950s, as American incomes trebled and US companies became the most powerful in the world, the Dow Jones entered a historic bull market. Between 1949 and 1956, the Dow Jones Industrial Average index gained 222%, going from 161.6 points in June 1949 to closing at 521.05 points on April 6, 1956. An estimated 10 million new investors rushing into the market to begin trading on Dow Jones companies during this period, many of whom made substantial gains. If one had invested $1000 in US Steel at the beginning of the bull market, they would have a $7000 investment by the end of it. If a trader had decided to invest $1000 in IBM in 1949, by 1961 that investment would have grown to $26,300. Few other periods in economic history have seen such returns.

Stagnation, Recurring Crises, New Horizons (1960-1990)

Much of the 1960s was a relatively quiet period for the Dow and is commonly described as a period where the index “went sideways”. This is because, while modest growth did occur across the index as a whole, the actual numbers were negligible compared to what had come before, whilst investor returns were close to non-existent. This is, of course, not true across the board. Major technology companies on the Dow at that time, such as United Technologies and IBM, saw their share price rise sharply over the decade, planting the seeds for America’s first tech stock boom. Meanwhile, while the Dow companies performed sluggishly, other indices paint a much rosier picture. The S&P 500, a much broader index of American companies, earned respectable returns of around 7% during the 1960s.

There are a number of reasons attributed to the poor performance of the DJIA during this period, with the most common being the out-of-control inflation rates experienced during this time, as well as the lack of dynamism among the established industrial giants listed on the index. Nonetheless, the 1960s were a quiet decade by the standards of the Dow, with little by the way of crashes and crises materializing.

However, anybody complaining about the lack of excitement on the Dow during the 1960s was likely feeling nostalgic for it by the time the 1970s were drawing to a close. As America and the wider world spiralled into a series of economic maelstroms, not least the OPEC oil crisis (1973), the Dow Jones index entered a particularly dark period. As US relations with oil-producing Middle Eastern countries worsened, the western world was hit with an energy crisis as supply hit a historic low. Only weeks prior to the crisis the Dow Jones surpassed the 1000-point mark, only to lose 48% of its value during the 1973-74 stock market crash, during which listed US energy giants such as Standard Oil, Texaco, and Exxon were particularly hard hit. It’s worth noting here that, although the Dow’s performance was poor, overseas indices such as the FTSE 30 fared worse, with the British index losing 73% of its value during the same period. Runaway inflation and low economic confidence in the US compounded matters for the Dow, meaning that, by the end of the decade, it had only recovered slightly, closing the 1970s at 838 points.

The 1980s were years of extremes in the Dow Jones index history, with huge levels of growth tempered by brief and dramatic crashes. The first half of the decade was largely abysmal, with the Dow breaking 1000 points every few months, only to fall back to previous levels shortly after. The period of 1984-87 was one of rapid growth, as deregulation and accelerating globalization propelled the DJIA companies to new heights, with the index peaking at over 2700 points in August 1987. However, this same deregulation allowed for many of the conditions to form that caused Black Monday on October 19, 1987, in which the Dow Jones saw its largest single-day percentage drop in history, losing 22.61% before closing. Similarly, other major indices were pummeled, with the S&P 500 and Wiltshire 5000 both losing just over 18% on the same day.

Even today, the reasons for the crash, which sparked fears of a return to the Great Depression, are not entirely known. Some blame the negative impact of inexperienced smaller traders distorting the market, while others blame the sale of financial instruments based on market price rather than on market fundamentals such as GDP or earnings reports. Despite all of this, as well as another mini-crash in 1989 and the disastrous Japanese Asset Price Bubble, the Dow ended the decade 228% higher than at the start of the 1980s, closing 1989 at 2752 points.

The Dot-Com Era, Short Sharp Shocks, and Record Heights (1990-2008)

The 1990s were a time of heightened optimism in the American economy, and this is reflected in the many Dow records broken during the decade. On January 2, 1990, the Dow Jones closed at 2810 points – then a record-high that encouraged plenty of cautious optimism among market pundits. However, even the most optimistic pundit could not have predicted what the Dow Jones would look like at the end of the decade. On March 29, 1999, the index closed at 10,006.78 points, capping off an unprecedented winning streak that saw trading floors on Wall Street erupt into celebration, with party hats and gallons of champagne at the ready.

So how did this remarkable bull market, which hasn’t been repeated before or since, actually come about? The economic boom of the 1990s has been analyzed by countless economic historians, all of whom have advanced their own theories to explain the upward trajectory of the market through the decade. Some attribute the growth to record-low oil prices, economic deregulation, and egalitarian income and corporate tax measures brought in by the Clinton Administration. Others attribute the boom to accelerating globalization, epitomized by landmark free trade deals such as NAFTA, which DJIA-listed exporting giants such as Johnson & Johnson, Wal-Mart Stores Inc., Merck & Co, and General Motors benefitted greatly from.

Perhaps most significant was the Dot Com Bubble, which dominated economic headlines during the latter half of the decade. While the impact of the bubble on the real US economy is debatable, it certainly had a disproportionate impact on the Dow, as well as other indices such as the S&P 500 and the NASDAQ Composite. The Dot Com Bubble was fueled by the proliferation of internet connectivity in the US and the birth of the Information Age, which led to widespread euphoria over what pundits were calling the ‘New Economy’. The birth of Silicon Valley as the global epicenter of tech occurred during the bubble, with household names such as Microsoft, Intel, and Hewlett-Packard entering the Dow Jones Industrial Index for the first time.

At the peak of the bubble, web companies such as Pets.com and WebVan had valuations hundreds of times higher than their actual balance sheet, whilst shares in newcomer tech companies like Qualcomm rose by more than 2500% in a single year. Of course, such an obviously over-heated market could not last forever, and the bubble burst spectacularly at the turn of the new millennium. Between 1999 and 2002, investors fled over-heated tech stocks in a mass flight that helped to fuel a major stock market downturn. Owing partly to the (then) less technology-oriented nature of the Dow Jones, it got through the bear market having lost “only” 27% of its value (this loss still represented over $1 trillion of market cap). However, the heavily tech-focused NASDAQ lost a staggering 75% of its value over the same period, going from 5000 points in 2001 to barely over 1000 points in late 2002.

The Great Recession and the Endless Bull Market (2008-2019)

The period between 2003 and 2007 was a rosy one for the Dow Jones, with virtually uninterrupted growth during this time leading to the index closing at a record high on October 11, 2007 of 14,198.10 points. However, the Financial Crash of 2007, precipitated by the US Sub-Prime Mortgage Crisis and the collapse of Lehman Brothers, sharply reversed these gains. As the global economy was thrown into economic turmoil unparalleled since the Great Depression, 2008 became the year that the Dow Jones saw its greatest ever single-day point loss, greatest ever single-day point gain, and largest intraday point range, before settling at a 12-year low of 6,547.05 points on March 9, 2009.

Despite the positive impact of the economic stimulus provided by the Obama Administration and the Federal Reserve as a response, the Dow Jones remained hampered by the jitteriness and trauma of investors for years afterward. Once-benign developments such as relatively weak US jobs report shaved hundreds of points off the Dow in a single day in June 2012 – a sign that investors were constantly worried that another Great Depression was just around the corner. The stock market didn’t recover until mid-2013, after which the foundations were in place for the most impressive bull market in the history of the Dow. While economic recovery on the ground has been weak since the crash, with wage growth and inflation at record lows, the Dow enjoyed a historic winning streak. Between 2015 and 2019, new records were broken on an almost daily basis, with much of the growth being propelled by tech giants such as Apple Inc. and Microsoft, both of which became some of the world’s first-ever publicly traded trillion-dollar companies during this period. Massive tax cuts and deregulation by the Trump Administration, much of which removed the constraints placed on the financial industry in the aftermath of 2007, also helped push the Dow up to record heights. On February 12, 2020, the Dow Jones closed at an all-time high of 29,551.42 points.

Coronavirus Chaos (2020-)

As you read this, it is likely that we are still experiencing one of the most seismic events in economic history. The coronavirus, also known as COVID-19, managed to spread to every corner of the Earth, with economies grounding to a halt and trillions of dollars being wiped off of the market caps of major indices and companies on every continent as a consequence of this.

As business closures forced millions of Americans onto unemployment rolls and massive sectors such as travel and hospitality collapsed overnight, the Dow was sent into a virus-induced tailspin. In the wake of the coronavirus, stocks in most major industries suffered. On March 16, 2020, the Dow Jones experienced its biggest point drop in history, losing 3000 points in a single day. Similarly, trillions of dollars were erased from the S&P 500 and the NASDAQ Composite, with the former faring the worst and losing more than 20% of its value on the same day.

DJIA listed companies in particularly vulnerable sectors bore the brunt of the downturn, with airplane manufacturer Boeing seeing share prices fall by more than 70% and McDonald’s Corp seeing the most dramatic drop in the company’s history. Companies that are better placed in a crisis of this nature, such as the pharmaceutical and medical giants Merck & Co and UnitedHealth Group, have been relatively unaffected, with both of their respective share prices recovering.

It is truly impossible to say how the Dow Jones stock exchange will perform over the coming weeks and months or how the coronavirus will continue to affect stock markets globally. We may see a major rebound, or we may only be at the very beginning of a protracted economic downturn that some have estimated may be worse than the Great Depression. Only time will tell. One thing that is certain is that anyone looking to buy and sell stocks on the Dow Jones is certainly in for interesting times ahead.

Recommended by DailyFX Research

Building Confidence in Trading

Is the Dow Jones Still Purely Industrial?

Source: Business Insider

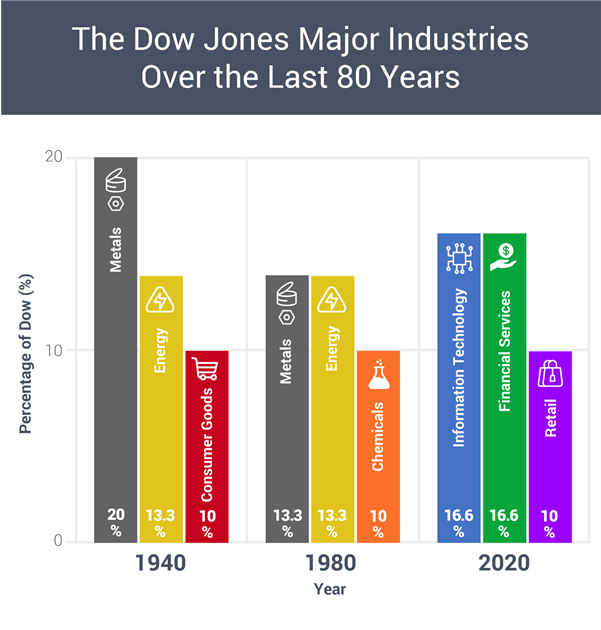

Compared to many other major stock indices around the globe, the Dow Jones Industrial stock market is more mercurial than most. While indices such as Germany’s DAX or Japan’s Nikkei have many members that have been listed since the inception of those indices, the DJIA currently has zero companies that were there from the start. In fact, even going back as recently as the 1970s, there are only three companies that have remained on the index today from that period; Exxon Mobil (formerly Exxon Corporation), Proctor and Gamble, and United Technologies.

In fact, if one was to look at the Dow Jones Industrial Average components today, they would likely conclude that the index does not look very ‘industrial’ at all. Although once dominated by titans of industry such as Standard Oil, US Steel, Allied Chemical & Dye Corporation, and General Motors, very few of the companies in the DJIA today have any connection to heavy industry.

In terms of index weighting, today the Dow Jones Industrial Average consists of ‘softer’ sectors such as retail, IT, and financial services, with Apple Inc., Home Depot, Visa Inc., and Goldman Sachs dominating the top of the pile. Given that the Dow represents the biggest players in the biggest economy in the world, changes in its composition strongly reflect changes in not just the economy and culture of the United States, but of the world. Let’s take a closer look at how the sectoral composition of the Dow Jones has changed, and what the forces behind these dramatic shifts are.

Dow Jones Veterans

ExxonMobil (Entered 1 October 1928): The multinational oil and gas corporation ExxonMobil began life on the DJIA as Standard Oil in 1928, then the company of the richest man in human history, John D. Rockefeller. The company has gone from strength to strength, climbing the DJIA to become the most valuable company on the planet several times during the course of its existence. Its first big expansion came in 1972, when Standard Oil of New Jersey absorbed Humble Oil to become Exxon Company, U.S.A.

Its biggest leap up the index came in 1998, when Exxon, the largest oil company in the world signed a $73.7 billion merger agreement with Mobil, the third-largest oil company in the world, cementing the biggest merger in history at that time. Today, ExxonMobil has cornered a large portion of the global oil, gas, and petroleum market, enjoying revenues of $279.3 billion in 2018 and assets totaling more than $346 billion.

Proctor and Gamble (Entered 26 May 1932): Proctor & Gamble, known as P&G for short, is a mammoth consumer goods conglomerate that operates some of the most well-known brands on the planet, including Ariel, Crest, Febreze, Gillette, Tide, and Vicks. Originally focused solely on cleaning products, P&G became one of the first international companies on the Dow when it acquired a major soap company in Newcastle Upon Tyne, UK, in 1930.

Since then, P&G’s sustained success has been largely due to its canny ability to identify emerging market trends, promptly snap up companies in those trend areas, and then market them highly effectively to an audience of billions. As well as acquiring rising starts such as Folgers Coffee, Pepto-Bismol, and Old Spice, they have also proven adept at developing their own smash-hit products, including low-calorie potato chip substitutes that are used around the world and the first-ever disposable diapers. Today, P&G remains the largest consumer goods company on Earth, with 2019 revenues of $67.68 billion and assets totaling $115.1 billion.

Raytheon Technologies (Entered 14 March 1939): Formerly known as United Technologies until its $100 billion ‘merger of equals’ with the Raytheon Company on April 3, 2020, Raytheon Technologies is one of the largest defense companies on the planet. Originally entering the Dow Jones index in 1939 as United Aircraft, the company rose to the upper echelons of American industry thanks to the near-limitless global demand for aircraft parts and aircraft during the Second World War.

After the war was over, United spent the following 80 years near the top of the Dow by manufacturing products for major US industrial projects and expanding its role as one of the world’s foremost military contractors. United Technologies remained a prominent member of the Dow right up until merging with Raytheon, a move which has likely cemented its position as a Dow lifer for decades to come. With more than 195,000 employees and projected revenues for $97.75 billion for 2020, Raytheon Technologies is likely to dominate the defense industry for the foreseeable future.

Dow Jones Newcomers

Apple Inc (Entered 19 March 2015): While it seems hard to imagine a world where Apple Inc. was not among the most valuable, profitable, and influential companies in history, this was not always the case. The company spent much of the 90s relegated to the role of bit player in the global IT arms race and didn’t return to profitability until 2007 with the launch of the first iPhone. After that the rest, they say, is history.

The mammoth success of the iPhone allowed Apple to position itself as the largest cellphone manufacturer on Earth, whilst leveraging the intense brand loyalty felt by customers to expand their offerings into home devices, smartwatches, cloud computing services, and video game platforms. Since Apple first entered the Dow in 2015, it has risen through the ranks to become one of the most valuable components on the index, comprising 8% of the total Dow Jones market cap. With 137,000 employees in dozens of countries, as well as 2019 revenues of $260.17 billion and a staggering $338.5 billion in assets, Apple Inc. is a giant of American business and a company that had made history countless times in its relatively short existence.

Visa Inc (Entered 20 September 2013): The astonishing success of Visa, finally culminating in a listing on the Dow in 2013, is a testament to the power that individual companies have to completely change the world. Visa first rose to prominence in the 1960s, financed by Bank of America, as the world’s first all-purpose credit card system, allowing a consumer to buy almost anything they wanted via a single credit transaction. Since then, Visa has expanded its operations beyond credit provision to become a vital component of the global financial system.

Today, 2.4 billion people use Visa credit or debit cards, it controls 50% of the global payments market, and facilitates the transfer of trillions of dollars between banks and countries every single day. Since going public in 2008, Visa shares have been immensely popular among investors, rising 22% since then as a result. There are few countries that can come close to competing with Visa, with only ChinaPay, a company focused mostly on its domestic Chinese market, having a larger number of customers. Last year Visa brought in over $20 billion in revenue, whilst commanding assets of almost $70 billion.

Goldman Sachs (Entered 20 September 2013): The multinational investment bank and financial services giant has always been synonymous with success, power, and wealth. However, it didn’t actually climb to the top of the pile and earn a place on the Dow until late 2013, despite being founded all the way back in 1869 – 151 years ago. The company has seen its valuation rise steadily for the first century of its existence thanks to savvy investments and acquisitions of some of the world’s largest and most promising companies.

In addition, Goldman Sachs’ size and expertise has meant that it has played a pivotal role in the economic history of the United States, with close to a dozen CEOs going on to work for the White House and the US Treasury, and the company itself has at different times both financed and been financed by the US government. Despite coming close to total collapse during the Financial Crash of 2007-8, Goldman Sachs today has bounced back and is stronger than ever. With 2019 revenues totaling $36.5 billion and an almost unrivaled $1.2 trillion listed on its asset sheets, Goldman Sachs clearly has the clout to continue shaping developments within the US economy for many years to come.

What Explains the Shift?

The American economy has clearly undergone a sea-change in the past century, which helps to explain why the Dow Jones Industrial Average has not looked like a listing of ‘industrial’ companies for many decades. The DJIA may not be the most representative snapshot of American business, but it most certainly is a reliable tally of the most successful companies in America today.

Gone are the manufacturing giants, industrial chemical companies, car producers and the rest, replaced by financial services providers, retail companies, and IT giants. In line with much of the rest of the rich world, the US economy has moved from being a largely manufacturing economy to a largely services-oriented one.

Today, the service economy represents almost 70% of US industry, whilst manufacturing only represents 11.6%, according to the US Bureau of Economic Analysis. Historical data on manufacturing is difficult to assess, but it is known that in 1953, around half of Americans worked in manufacturing and heavy industry jobs, compared to just 8% today. This shift helps explain the changing constitution of the Dow Jones, and the reasons for it are myriad.

Globalization has shifted manufacturing to the Global South, owing in part to lower labor costs. The USA’s high level of development and education have promoted the rise of high-technology and knowledge-focused enterprises. The strong IP laws in the US have been conducive to service-oriented businesses.

The list goes on and on. Of course, America remains a manufacturing powerhouse, with the industrial sector generating $2.2 trillion last year, but the gap between services and manufacturing is likely to grow significantly wider in the years and decades ahead.

Recommended by DailyFX Research

Traits of Successful Traders

Dow Jones and the White House

Source 1: Macro Trends

Source 2: Investopedia

The Dow Jones components invariably have an outsized role to play in the US economy, and always have done. It is therefore unsurprising that the actions of various US presidents over the years have in turn had a sizeable impact on the Dow Jones and companies listed on it. The White House, with the US President at its center, has the power to draw up the Federal Budget, sign-off on economic stimulus packages, appoint directors to the Federal Reserve, and push through dramatic economic policy changes via executive order. Just as every other feature of American life has been closely impacted by who is in the White House, the business landscape and the fortunes of the Dow Jones are closely connected to the current Administration. Let’s take a closer look at the past four US presidencies to see how the Dow Jones and specific companies have been directly affected by decisions taken by the Leader of the Free World.

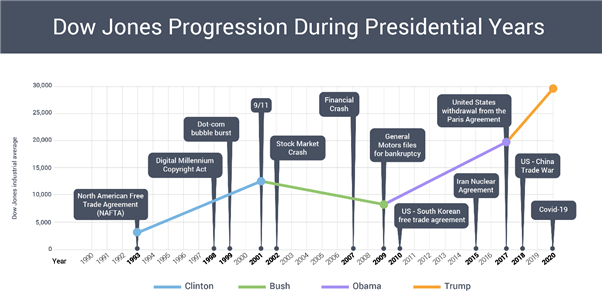

Clinton Presidency

Dow Jones Index at start of Presidency (January 20, 1993): 3241.95 points

Dow Jones Index at end of Presidency (January 20, 2001): 10,587.59 points

In percentage terms, the Clinton presidency represents the most significant period of growth for the Dow Jones Industrial Average, with the index more than tripling during Bill Clinton’s time in office. While Clinton’s time in the White House coincided with seismic Dow Jones news events such as the Dot Com Bubble, the administration also played a key role in the skyrocketing fortunes of the DJIA during this time.

Perhaps most significant in policy terms was the ratification of the North American Free Trade Agreement (NAFTA) in December 1993, which had been painstakingly negotiated by his predecessor and himself. In addition, the Clinton Administration greatly assisted major multinationals on the Dow by signing over 300 international trade agreements, most notably with China, the EU, and newly capitalist Russia.

During this time Dow members such as Chevron, and Exxon saw their share prices triple, whilst consumer goods exporters such as Coca Cola and Walmart actually saw their share prices rise more than ten-fold during Clinton’s tenure. The first major IT companies to enter the Dow – Microsoft, Hewlett-Packard, and Intel – did so during the Clinton years, helped along by landmark pieces of legislation such as the Digital Millennium Copyright Act, which greatly increased the power of tech platforms to generate and protect revenue streams.

Perhaps most importantly, Clinton presided over a significant period of economic deregulation, particularly within the telecommunications and financial industries, to the significant benefit of the largest market players. The trading of financial products such as derivatives was virtually completely deregulated with the Commodity Futures Modernization Act, whilst Clinton’s Gramm-Leach-Bliley Act removed broad swathes of requirements for financial services providers.

This helps to explain why Dow-listed financial giants such as American Express Company and Citigroup Inc greatly expanded their operations and saw the share prices rise dramatically during the Clinton admin, from $7 to $40 and $59 to $550 per share respectively. Overall, the Clinton Administration is largely remembered as a golden period for the economy and representative of the ‘Golden Age of Globalization’ that saw multinationals benefit like never before.

Bush Jr. Presidency

Dow Jones Index at start of Presidency (January 20, 2001): 10,587.59 points

Dow Jones Index at end of Presidency (January 20, 2009): 7949.09 points

Despite beginning his presidency during the worst years of the Dot Com crash and having to quickly weather the US economy through traumatic events such as 9/11, George W. Bush was able to keep the economy out of a recession for the first few years of his presidency. His final months in office are largely overshadowed by the Financial Crash and the significant economic fallout from that which saw the Dow lose thousands of points in the last six months of the Bush Administration.

Before the crash, growth was hardly stellar, but a then-record high of 13,442.52 points was reached in September 2007, just weeks before the crash. Very few major trade deals were signed or ratified during Bush’s tenure, save for the ‘Dominican Republic-Central America Free Trade Agreement’, which did little to benefit America’s biggest companies (although Coca Cola, with its bottling plants and refineries across Central America, was reportedly a keen proponent of the deal).

There were several major tax cuts made during the Bush admin, although it is generally agreed that any benefit to businesses was largely offset by the re-introduction of protectionist tariffs that had previously been scrapped by the Clinton Admin. One example is the 2002 United States Steel Tariff, designed in part to offset competition from China, which entered the WTO for the first time in 2001.

Rather than focusing on economic stimulus, the Bush Admin was largely focused on ramping up defense spending after the invasion of Iraq, trying to bring down skyrocketing levels of national debt, and, finally, administering trillion-dollar bailouts to banks and financial institutions during the height of the Great Recession.

Although much of the Bush period was a relatively rosy period for the economy, policy in this area was decidedly unambitious, due to other issues sucking all of the oxygen out of the room. Of the few winners from the Bush admin that are on the Dow, defense and energy companies made out the best, with United Technologies, Exxon Mobil, Boeing, and Chevron seeing the biggest gains as a direct result of White House policy.

Obama Presidency

Dow Jones Index at start of Presidency (January 20, 2009): 7949.09 points

Dow Jones Index at end of Presidency (January 20, 2017): 19,827.25 points

Few people would disagree with the notion that Obama was dealt a tricky hand upon assuming the Presidency in 2009, with the economy mired in the worst downturn since the Great Depression and the Dow on a seemingly irreversible downwards trajectory. However, Obama managed to reverse the decline and oversee the largest points increase in the history of the Dow, with 12,000 points added to the index during his tenure.

In addition, US corporate profits reached their highest levels in recorded history by mid-2014, whilst the S&P 500 set new record highs a total of 118 times during the Obama Presidency. By all accounts, it was a good eight years for the Dow and the vast majority of companies listed on it.

Part of this is directly related to White House policy, not least the record-breaking economic stimulus packages that were introduced in order to jolt the economy back to life. Huge support packages for industries such as energy, finance, healthcare, and manufacturing brought the US’s trade deficit down to one of its lowest levels ever, whilst Obama’s waiving of energy export ban saw companies such as GE and ExxonMobil become some of the biggest energy market players on the planet.

Meanwhile, Dow newcomers such as Nike, Apple, Visa, UnitedHealth, and Goldman Sachs reflected the heightened power of American service providers on the global stage, helped in part by sweeping trade deals agreed with countries such as South Korea, Japan, Columbia, and Panama. There were, of course, some casualties during the Obama years – most notably General Motors, which filed for bankruptcy in 2009 and exited the Dow that same year after almost 100 years on the index.

The Obama Admin kept GM afloat with low-interest loans in order to protect its hundreds of thousands of US employees, but it never returned to its former glory. Overall, the Obama years were most notable for record corporate profits and the ascendancy of big tech onto the Dow, thanks in part to the administration’s notoriously friendly attitude to Silicon Valley.

Trump Presidency

Dow Jones Index at start of Presidency (January 20, 2017): 19,827.25 points

Few US presidents have galvanized public opinion like DJT, but there is little denying that few other presidents have had such a direct impact on the US economy than this individual. Much of Trump’s economic policy has centered around US protectionism and promoting American business, a position exemplified by landmark policies such as the re-structuring of NAFTA to better suit US interests and, of course, the US-China Trade War.

Trump certainly inherited a positive economic situation from Obama, which in part explains why the Dow Jones highest close ever of 29,551.42 points was reached in February 2020, at the peak of the most extensive bull market in US history. Corporate profits continued to rise during the Trump Admin, helped in part by his sweeping $1 trillion tax cut that largely benefitted America’s biggest companies, thus pushing the Dow to dizzying new heights.

On a more micro level, there are a number of individual actions taken by Trump that have had an immediate and dramatic impact on the Dow. Trump’s withdrawal from the Paris Climate Agreement facilitated the return of America as the world’s largest oil producer for the first time in decades, with ExxonMobil, Chevron, and Caterpillar Inc. all seeing significant share price gains in the aftermath of the withdrawal.

Of course, Trump’s trade wars with China and smaller trade conflicts with countries such as France, Canada, and Mexico have negatively impacted some companies which rely heavily on international sales, namely Apple Inc. and Nike, but overall it seems that the Trump Presidency has, so far, been good for the Dow and its constituents.

Of course, with the COVID-19 virus now causing the most significant recession in decades and forcing thousands of US companies to close their doors for the time being, the verdict on the Trump Presidency could look very different by the time he leaves the White House.

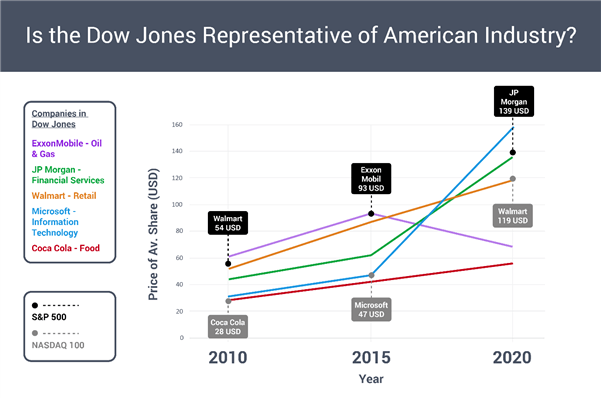

Does the Dow Jones Represent the US Economy?

Source 1: Business Insider

Source 2: Business Insider

Source 3: Business Insider

Despite its central position in American culture, the most common criticism leveled against the Dow Jones Index is that it is not representative of the US economy at large. Some of the largest and most influential companies in America, including Alphabet (the parent company of Google), Amazon, AT&T, PepsiCo, and Blackrock, the latter of which controls $7 trillion in assets, are not listed on the Dow Jones.

They are, however, featured on the other main stock indices in the US; the S&P 500 and the NASDAQ Composite. Part of the reason that these companies, some of which have greater valuations than companies on the Dow, are not listed there is because of the way that the Dow is calculated. The Dow places a disproportionate (as some have argued) weight on the price of the individual stocks.

Furthermore, owing to the Dow’s origins, more weight is afforded to companies from traditional industries such as energy. Although this tendency has gone into reverse over the past couple of decades, as we have seen, it helps to further explain why so many massive global companies have never been included on the Dow Jones Industrial Average.

Despite this exclusion, it does not necessarily mean that the common accusation that the Dow is no longer representative holds true. One of the central tenets of the Dow, as frequently exclaimed by its proponents on Wall Street, is that the performance of the 30 massive companies on the index can be very helpful in shining a light on the broader economy. The theory generally goes that, if the companies with the most significant presence in the US economy are performing well or poorly, the same can generally be said of other companies.

To get the whole picture, it helps to compare the Dow Jones with the other major stock indices of the US economy to see what the strengths and weaknesses of each really are. Let’s take a closer look at how the Dow Jones, S&P 500, and NASDAQ compare to each other.

S&P 500 vs the Dow Jones Industrial Average

In conversations about the value of the Dow Jones in 2020, the S&P 500 index is most frequently cited as a more reliable alternative when attempting to chart out the health of the American economy. Founded in 1957, the S&P 500 Index is, rather broadly, described as an index of “500 large publicly-traded American stocks”. While this may seem like a rather broad definition, there are further indicators that determine whether a company is worthy of a listing on the index.

Most importantly, they must have a market cap of at least $8.2 billion (as of 2020), which already excludes the vast majority of large US enterprises. In addition, it must have a public float (number of shares owned by public investors) of 50% at the very least. It must also have positive revenues for the past four quarters to remain on the index, meaning that any company that contracts during a single quarter will promptly be booted off of the S&P 500 index.

The crucial distinction that separates the S&P 500 from the Dow Jones, other than the fact that it is much more inclusive, is that components are weighted by the market cap, rather than their stock price like they are on the DJIA. Companies on the S&P do not need to be blue-chip, which explains why many market hawks consider the Dow Jones to be a more reliable indicator of quality companies rather than merely profitable ones.

Investor reputation is incredibly important, and blue-chip status is a widely respected indicator of this. When attempting to gauge the standing of the US economy, it is understandable to focus on the companies that enjoy the best reputation among investors. However, it is worth noting that many of the largest companies on the S&P 500 are blue-chip components anyway, such as Apple Inc., Alphabet, and Mastercard Inc.

In terms of industries, the S&P 500 and Dow Jones have broadly similar compositions, with technology and industrials both making up a significant chunk of the indices. However, the S&P 500’s criteria mean that there are some key distinctions in this regard. For one, the S&P 500 gives greater inclusion for financial companies, which is why major institutions with massive market caps such as Bank of America, Capital One, Wells Fargo and MetLife, some of which have larger market caps than some companies on the Dow, are included on the S&P.

Since the Dow Jones claims to be an index of the top 30 American companies, it makes sense to look at the top 30 ranked companies on the S&P 500 to see if there are any disparities. Here, there are some revealing distinctions. Several companies listed on the Dow do not feature anywhere near the top 30 S&P 500 companies in terms of market cap. These include Boeing (listed at #70 on the S&P), Caterpillar Inc. (#82), Travelers Companies (#171), Nike (#50) and Chevron (#31).

It is clear that both indices value very different things, which reflect the respective representativeness of both. Of course, it’s worth noting that if you were to place a line graph of the S&P’s performance over the past 50 years next to a graph for the Dow’s performance over the same period, the trajectory is virtually identical.

NASDAQ vs the Dow Jones Industrial Average

The other major US stock index that is broadly considered to be a barometer for the wider economy is the NASDAQ Composite. Remember, the NASDAQ Composite is a separate entity to the NASDAQ. The NASDAQ is an electronic exchange that allows people to buy and sell shares, while the NASDAQ Composite is an index of 3300 stocks that trade on the NASDAQ.

Other than the fact that the NASDAQ Composite tracks more than 100 times as many companies as the Dow Jones, the most important distinction is that it focuses mostly on technology companies, with the majority of listings coming from the tech sector. In addition, companies listed on the NASDAQ Composite do not have to be based within the United States, but it must be listed in the US on the NASDAQ stock market.

In reality, virtually all of the major NASDAQ listings are US companies, with a few exceptions of the likes of Baidu (China) and Liberty Global (UK). The majority of the NASDAQ Composite’s movements are focused on the NASDAQ-100 which, as you may have guessed, is an index of the NASDAQ Composite’s 100 largest companies.

This index is weighted almost entirely by market cap, with a few restraints in place to prevent the largest players from having an outsized influence on the performance of the index. It consists entirely of non-financial companies, with finance components related to a separate index called the NASDAQ Financial-100.

The NASDAQ’s heavy focus on technology companies means that it has historically been much more volatile than the Dow Jones, given the high boom and bust rate of tech giants. It has also, despite the constraints put in place, been accused of allowing the top-listed companies like Apple, Amazon, Alphabet, and Facebook to over-represent the index and distort its performance metrics considerably.

The NASDAQ does have some advantages over the Dow Jones, some of which can be revealed by looking at some of its top components that do not feature in the Dow, despite being in the NASDAQ’s top 30 by market cap. These include economic giants that have market caps larger than most countries, such as Amazon, Comcast, Adobe, Costco, and Facebook.

Given that these companies hold pivotal positions in the US economy and are among the largest employers in the country, their lack of inclusion on the Dow makes it is tempting to question whether it is still fit for purpose in 2020.

Strengths of the Dow Jones Industrial Average

While there is a lot of debate on which index is the most reliable for anyone wishing to gauge the economic situation, there is no denying that the Dow Jones offers some distinct advantages that the S&P 500 and the NASDAQ Composite do not. The most important advantage is arguably the standards that are set by the Dow, which are much higher than any other index.

The Dow exclusively tracks blue-chip stocks, which helps to guarantee that the companies it measures are undisputed leaders in their respective industries. This means that there is a reduced chance of individual cases of mismanagement distorting the wider stock market. It also means that the direction that these companies move in can broadly be used to indicate the direction that all companies within that same industry are headed.

The data seems to bear this out; if you were to compare the Dow Jones with the much more inclusive Russell 2000 index or the S&P 500 and you will see remarkably similar fluctuations. This strongly suggests that the unique weighting criteria favored by the Dow are effective enough for 30 companies to paint a highly reliable picture of the economy.

While there have been broad differences between the performance of the Dow relative to other indices, there are no major historical examples of the Dow diverging significantly from those indices in an unrepresentative or misleading manner.

Some have also argued that the Dow’s stock price weighting is more useful as it avoids the pitfalls over over-inflated ‘unicorn’ companies distorting the stock market, which is exactly what happened with the NASDAQ Composite during the Dot Com Bubble, which saw much more extreme losses than the Dow once the bubble burst.

Perhaps the biggest strength of the Dow is simply its reputation. It has been and remains the gold standard of economic indicators. When economists, politicians, bankers, traders, and journalists talk about the latest fluctuations in the ‘stock market’, they are most likely talking about the Dow Jones Industrial Average.

The high levels of trust and prestige bestowed on the Dow Jones gives it an edge as an economic indicator that the S&P and the NASDAQ simply cannot compete with.

Weaknesses of the Dow Jones Industrial Average

While the Dow Jones may be the most trusted index, it does have a number of not-insignificant shortcomings that other major indices do not suffer from. For one, while some prefer the Dow’s reliance on stock price when weighting components, others point out that such weighting exposes the index to an intense vulnerability.

Focusing on nominal share price can and has resulted in components being given weighting that is completely disproportionate to their actual economic value. This helps to explain why companies with relatively minimal value and influence such as Travelers Company occupy a prime position on the Dow, whilst languishing near the bottom of other indices.

It also explains strange situations such as Boeing’s Dow Jones Industrial Average massive weighting (at least prior to the coronavirus outbreak) on the index despite its relatively minor market cap. Another common criticism concerns the composition of the Dow, which excludes a number of crucial industries that are likely to form a crucial part of most stock investor portfolios, including utilities, a sector that is explicitly banned from the Dow.

Put simply, the Dow Jones is much less diversified than other indices, which some see as a handicap in an economic and investment landscape that is more diverse and Balkanized than ever before. Of course, some believe that the value of diversification is minimal past a certain point when it comes to comparing indices, especially if the components of an index already play a decidedly pivotal role in the wider economy.

Although the Dow Jones has, for example, included IT giants such as Apple onto the index in recent years, this is not really sufficient enough to reflect the current importance of the high-tech sector in the contemporary US economy. While some see the Dow Jones’ exclusivity as its greatest strength, others see it as a major weakness that leads to poor levels of overall representation when attempting to gauge the economy on a macro level.

Recommended by DailyFX Research

Traits of Successful Traders

Dow Jones vs The World

As the most respected index of the top companies of the largest economy on the planet, the Dow Jones Industrial Average has a reach that extends far beyond the shores of the United States. This is exemplified by the fact that traders in every corner of the globe buy and sell Dow Jones stocks today.

Whenever there are significant ups and downs in the global economy, media outlets in virtually every country take stock of the position of the Dow Jones to assess the scale and nature of developments on a global scale. The fact remains that when America sneezes, the global economy catches a cold. The companies listed on the Dow Jones typically have a significant influence abroad, employing people in dozens if not hundreds of countries and occupying a critical position in global supply chains.

The US and its businesses also represent the world’s largest consumer market by a considerable margin. As such, the Dow Jones in, in several respects, a global stock index. However, that does not mean that it is the only game in town. Other major global stock indices, some of which are calculated and weighted in a very different way to the Dow, are considered by some to be an equally important measure of the global economy. Let’s see how the Dow Jones stacks up against some of the other major stock indices from the world’s major economies.

FTSE 100 vs Dow Jones Industrial Average

The FTSE 100 index is the leading index of the UK stock market, representing the top 100 companies in the UK that are listed on the London Stock Exchange. Components are included and weighted according to market cap, which distinguishes it from the stock price-based components on the Dow Jones. The total market cap of the FTSE 100 was around $2.55 trillion in January 2020, compared to $8.33 trillion for the Dow Jones.

Given that the FTSE represents more than triple the number of companies that the Dow does, it’s clear that the top US companies carry much greater economic weight on an individual level than British ones do. Nonetheless, some of the largest companies on Earth are still represented on the FTSE, including Unilever, Royal Dutch Shell, AstraZeneca, and HSBC, all of which carry assets worth hundreds of billions of dollars and have revenues that dwarf those of some companies listed on the Dow.

In terms of industry representation, the FTSE and the DOW are broadly similar, with finance, technology, oil, and pharmaceuticals dominating. However, the FTSE differs in that it also gives considerable weighting to companies in the aerospace, insurance, and media industries, owing to the outsized role these industries play in the economy of the United Kingdom.

One could, therefore, argue that the FTSE is more inclusive of different sectors and therefore more representative of British industry that than Dow is of American industry. However, this inclusivity is largely due to the weighting criteria of the FTSE, combined with the fact that these industries, which are much more marginal in the US when it comes to GDP, are much more central in the UK. In 2019, the FTSE 100 grew 12.10%, compared to 22.34% for the Dow Jones Industrial Average.

NIKKEI 225 vs Dow Jones Industrial Average

The Nikkei 225 is the leading stock index of Japan, the world’s third-largest economy and one of the most influential players in global trade. The Nikkei tracked the leading companies that are listed on the Tokyo Stock Exchange, the largest stock exchange on Earth. Interestingly, the Nikkei is weighted in much the same weight as the Dow, using a price-based system that is

focused exclusively on blue-chip stocks. The Nikkei’s total market cap, though smaller than the Dow, is still formidable, standing at around $4.49 trillion in January 2020.

The Nikkei has many of the best-known Japanese companies at the top of the index, including Canon, Sony, Toyota, Mitsubishi, and Casio. Much like the Dow, technology companies feature prominently on the Nikkei. However, given that high-tech, particularly in the form of electronics, has been a large part of the Japanese economy for much longer than it has been in the US, this industry has much greater representation on the Nikkei.

Perhaps most strikingly, the Nikkei 225 is much more industrial than its US counterpart, owing largely to the central importance of Japan’s manufacturing sector. Unlike in the US, where manufacturing constitutes a mere 11.6% of America’s economic output, it makes up around 24% of Japan’s. This places Japan as the country with the third-highest manufacturing output on the planet, explaining why the Nikkei looks much more ‘industrial’ than the DJIA does.

The major industries represented on the Nikkei 225 are electronics, heavy industry, auto manufacturing, construction, chemicals, and food & beverages. There are some major financial institutions listed on the index, such as Softbank and Credit Saison, they play a much smaller role in the weighting of the Nikkei than they do on the Dow. Given that the Nikkei is more inclusive than the Dow, in that it lists 225 companies, it would be tempting to describe it as a more broadly representative barometer of the economy.

However, it is also worth noting that the Nikkei is calculated and weighted in virtually the exact same way as the Dow. In addition, while the US has competitor indices like the S&P 500, the Nikkei is, by and large, the only game in town for Japanese market watchers. Much like the Dow, the Nikkei is a prestigious, greatly respected national icon with a rich historic pedigree. In 2019, the Nikkei grew 18.2%, compared to 22.34% for the Dow Jones year to date growth.

Conclusion

Regardless of where you stand on the Dow, there is no denying that it represents the crème de la crème of the US economy. Companies with large valuations come and go, which is why the Dow prefers to focus on companies that best represent the innovation, trustworthiness, originality, and ambition that define all that is great about the American economy and the American Dream.

Recommended by DailyFX Research

Traits of Successful Traders

|

|

Leave a Reply

You must be logged in to post a comment.