S&P 500, DAX 40, FTSE 100 and Nikkei 225 Fundamental Forecast Talking Points:

- Seasonality likely plays a significant role in the S&P 500’s and other major indices’ recent rebound, but structural issues remain

- There is a confluence of systemic fundamental issues weighing the major equities markets lower, but the quickly deteriorating growth forecast is a top concern

- Monetary policy should be considered just as effective and onerous a threat to the market with central banks committed to hikes despite capital market struggle

Fundamental Forecast for S&P 500: Bearish

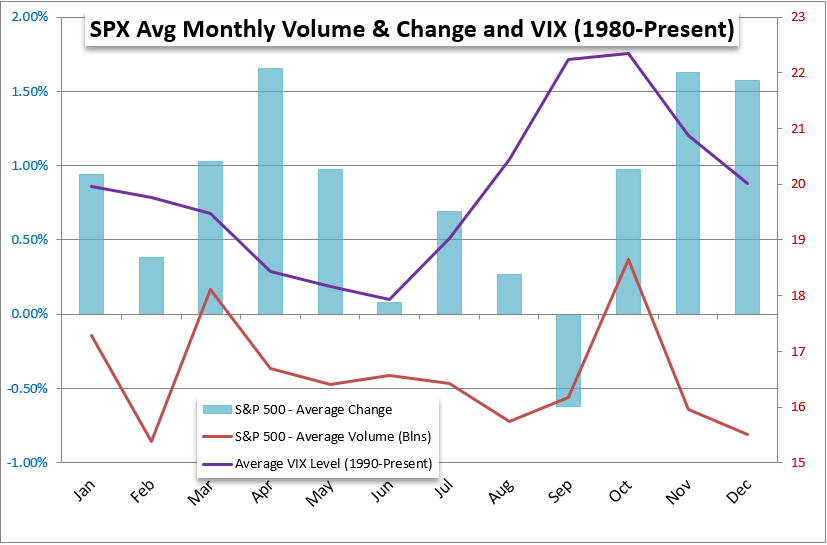

After seven straight weeks of bearish slide, the S&P 500 has finally found some semblance of balance with a relief rally. This could be the start of a significant reversal after the longest unbroken tumble since March 2001, but I consider it far more likely to be a temporary bounce. From a statistical basis, June is one of the weakest months for performance of the calendar year with the early start of the summer doldrums bringing on a significant slump in activity levels. Normally, that would be a favorable factor, but it isn’t a strong feature when the fundamental backdrop is overwhelmingly difficult and requires strong conviction to override the momentum. On the fundamental side, the conditions are onerous. We have passed through earnings season, and that leaves us with more persistently troublesome macro issues. The outlook for economic activity has deteriorated sharply since the IMF warned the world’s largest economy would suffer alongside the rest of the world. On the growth front this week, key event risk in the ISM manufacturing and services surveys will serve as strong proxy to GDP. Otherwise, the Conference Board’s consumer sentiment survey and Friday’s May NFPs will reflect on the US consumer – one of the strongest forces in the global economy.

Chart of the Historical Average Performance of S&P 500 and VIX by Calendar Month

Chart Created by John Kicklighter with data from S&P

Fundamental Forecast for DAX40: Bearish

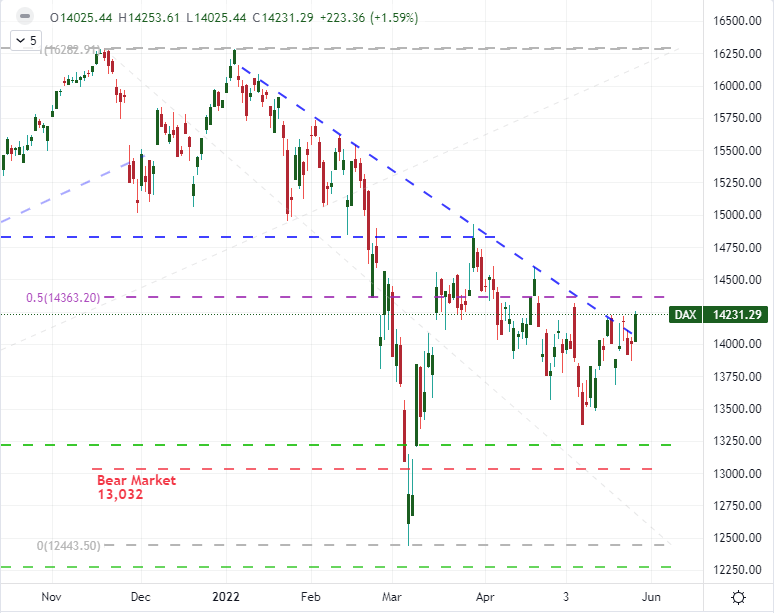

Though the German DAX 40 index is not far removed from its own official ‘bear market’ (defined by a 20 percent correction from all-time highs), its progress both lower and its recovery has been far more choppy than what has been seen in its US counterpart. In the macro themes that matter, the situation for this benchmark European measure are far more problematic than the same peer. The question is whether these issues continue to weigh in the coming week or they take longer to unfold. From a growth perspective, the outlook for Europe has been one of the most fraught with groups like the IMF highlighting the exposure to energy issues related to the Russian invasion of Ukraine as just one prominent factor. The Eurozone sentiment surveys could tap into that theme. Perhaps even more problematic is the struggle with hawkish ECB policy. The group has only recently signaled clearly that hikes are coming with President Lagarde saying the benchmark rate is likely to return to positive by the end of September. With the Eurozone and German CPI stats on tap, the market may continue to build up its expectations to something more commensurate with US, Canadian or UK counterparts.

Chart of German DAX40 Index (Daily)

Chart Created on Tradingview Platform

Fundamental Forecast for FTSE 100: Neutral

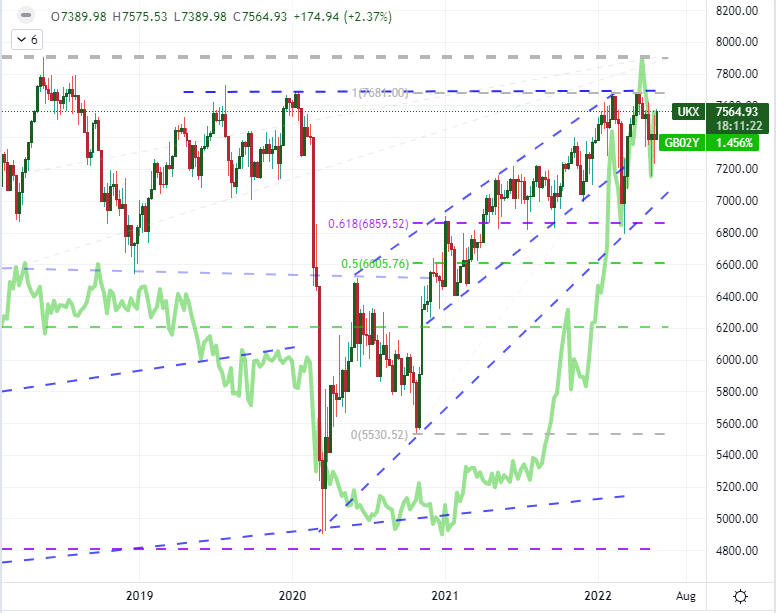

When is no news, good news? When the prevailing momentum has been negative for the capital markets, as it has been for most of 2022. Despite the slide in risk trends across the board, it is worth noting that the UK’s FTSE 100 index has managed far greater balance than most of its major counterparts. In economic potential, the United Kingdom’s downgraded 2022 outlook (by the IMF) was almost as severe as what befell the Eurozone – a 1.0 percentage point drop to 3.7 percent. Further for monetary policy, the Bank of England has move early and consistently to increase the financing burden on the economy. Nonetheless, the FTSE 100 hasn’t even printed a daily close into a ‘technical correction’ – a 10 percent retracement from cycle highs. While there are meaningful fundamental events over the coming week, there isn’t much in the way of systemically important updates. That breathing room along with the extended holiday weekend starting on Thursday could help provide this market some relief. That said, I don’t see these circumstances as particularly conducive to a genuine bullish backdrop.

Chart of UK’s FTSE 100 Overlaid with UK 2-Year Government Bond Yield (Weekly)

Chart Created on Tradingview Platform

Fundamental Forecast for Nikkei 225: Neutral

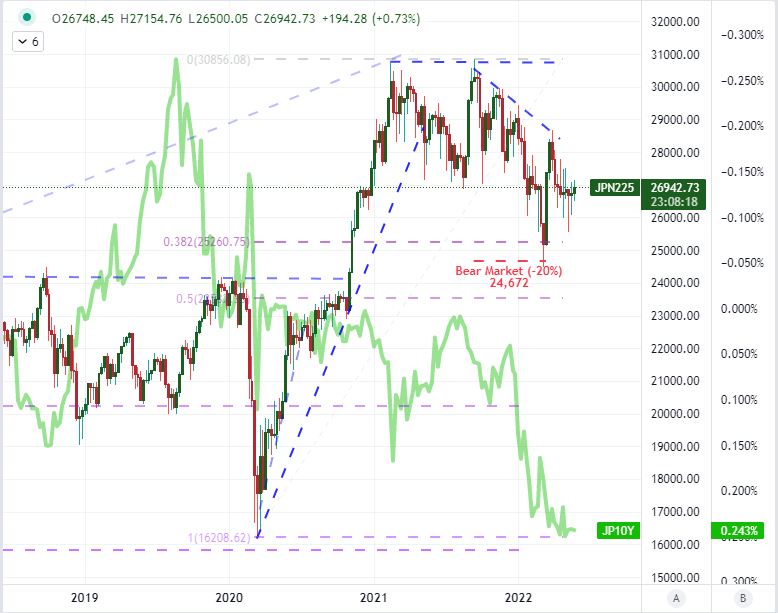

The Bank of Japan and its Governor Kuroda have committed to extraordinary stimulus to support the Japanese economy even when the other major policy groups around the world have moved to explicit and strong hawkish regimes. That doesn’t help the country much with a rise in inflation pressures, but it does represent a boon to the Nikkei 225. The equity index has not escaped the pressure exacted across the world as higher commodity prices have taxed imports and growth potential while the slowdown in major trade partners like the US and China represent a serious curb in export potential. However, there are fewer measures this week that will play to that particular threat. On the Japanese docket, there are a few meaningful updates including 1Q capital spending, April retail sales, industrial production and unemployment. These are unlikely, however, to carry the full weight of the market to a clear move whether bullish or bearish.

Chart of Japan’s Nikkei 225 Overlaid with Inverted 10-Year JGB Yield (Weekly)

Chart Created on Tradingview Platform

|

|

Leave a Reply

You must be logged in to post a comment.