US DOLLAR, JAPANESE YEN, COVID-19, CLO MARKET, FED OUTLOOK – TALKING POINTS

- US Dollar, Japanese Yen demand may swell on CLO market volatility

- Fed tapering, interest rate rise could pressure sensitive credit markets

- LIBOR to SOFR switch, COVID outlook remain major year-end risks

Hunt for Yields Boosting CLO Demand

After the market implosion in March 2020, the cost of credit briefly spiked across the financial universe as a reflection of the increased risk facing debt holders. However, aggressive Fed policy in the form of multi-trillion dollar bond purchases pressured yields lower and helped restore a sense of confidence.

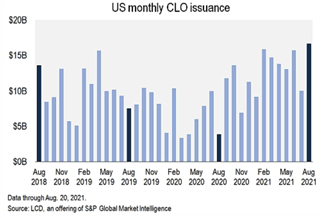

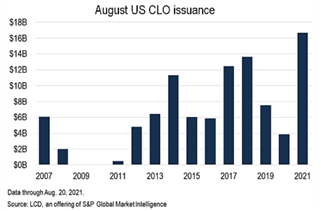

However, as sentiment recovered, so did the demand for interest income. The market for collateralized loan obligations (CLOs) then drastically inflated due to the comparatively higher returns they offered in a prevailing market of low – and sometimes negative – returns in comparatively safer, more traditional corners of the market. Fast forward 17 months and monthly CLO sales reached a 10-year high at approximately $18.6 billionin August 2021.

Source: S&P Global Market Intelligence

In short, a CLO – not to be confused with a CDO – is security which is backed by a pool of low-grade corporate loans. A more detailed explanation can be found in my report here. Prior to the pandemic – when interest rate conditions were also still accommodative but not to the same extent as they are now – CLO issuance was rising.

However, the quality of the loans that were being packaged into CLOs were rated close to “junk”. A more in-depth report can be found here, but in essence, these instruments were able to flourish because firms had access to easy credit. Banks were eager to lend, and corporations were anxious to take advantage of cheap capital.

A often-heard critique is that – as a result – firms became addicted to and dependent on cheap credit, relying on it more than economic fundamentals. This alleged divorce from reality created a risky situation in the event that the proverbial music stops (i.e. ultra-accommodative credit conditions end), and reality comes knocking. So, who then will be at the door?

Fed Policy Poses Significant Risk

For the past several months, investors have been watching the Fed very closely to pick up on any subtle cues that hint at tapering bond purchases and future rate hikes. At the most recent FOMC meeting on September 21, Chairman Jerome Powell said that officials intend on “[keeping] interest rates at zero and [continuing] the current pace of asset purchases”.

For CLO managers and sellers, Powell in essence turned up the music and told them to dance harder. Not surprisingly, the spreads on credit default swaps for sub-investment grade corporate debt fell that day, reflecting a less-urgent risk of tightened credit conditions. Having said that, the longer-term outlook does identify risks toward the end of 2021 and in 2022.

Mr. Powell added that “a gradual tapering process that concludes around the middle of next year can be appropriate”. While officials cut their growth outlook for next year – giving some respite to liquidity-dependent assets to the extent that this translates into easier credit conditions – inflation has been higher than expected. This may complicate future policy if growth is still lagging.

As of September 27, Fed funds futures indicate that market participants assign a 76.1% probability of at least one rate hike by December 2022. The probability of an increase by November is pegged at 54.5 percent, while the chance of a move before then is assigned less-than-even odds. Looking ahead, if economic data severely underperforms – perhaps on account of the lingering COVID-19 outbreak, or some other catalyst – the tightening timeline will likely get pushed out.

LIBOR to SOFR Switch on the Horizon

The London Interbank Offered Rate (LIBOR), a benchmark interest rate that underpins trillions of dollars’ worth of financial contracts, is set to be retired at the end of the year. Its replacement will be the Secured Overnight Financing Rate (SOFR), a relatively new mechanism developed by the Federal Reserve Bank of New York in April 2018.

The novelty of this new rate-setting benchmark could be a catalyst for notable volatility in the CLO market. According to the Wall Street Journal, “some CLO documents lack language covering the changeover to a new interest-rate benchmark, which could spark disruptions as the new year approaches”.

Legal changes in the documents underpinning CLOs that tie the new benchmark rate to SOFR rather than LIBOR may be a key source of friction. Consequently, while the degree of volatility from this single factor is unclear, the constellation of risks from COVID-19, the evolving Fed policy outlook, and this adjustment compound the risk of elevated year-end price moves.

How might traders hedge against this risk?

US Dollar, Japanese Yen May Rise on Credit Crunch Risks

As we saw in March 2020, credit spreads widened to biblical proportions as the perceived and actual risks of default on corporate debt surged. In this panic-ridden environment, the demand for havens like the US Dollar and anti-risk assets like the Japanese Yen surged. It is possible that a similar dynamic may ensue if the CLO market undergoes a bout of panic.

Traders may therefore cycle sentiment-sensitive assets out of their portfolio and divert their funds to currencies that have a tendency to perform well under stress. The US Dollar may become a particularly attractive choice if Fed commentary and economic data also strengthen the case for interest rate hikes, thereby giving the Greenback a relative yield advantage over its counterparts.

Year-to-date, the US Dollar has had the fourth-best interest rate returns, but the Greenback’s placement may gradually rise. Not surprisingly, the New Zealand Dollar, Norwegian Krone and Canadian Dollar all outperformed USD in large part due to their cycle-sensitive nature, allowing them to prosper in a risk-oriented environment. This dynamic, however, may reverse.

For more market analysis, be sure to follow @ZabelinDimitri on Twitter

|

|

Leave a Reply

You must be logged in to post a comment.