Simon Property Group (NYSE: SPG) has recovered significantly from its mid-March lows as one of the largest commercial REITs in the country. The company’s more than $20 billion market capitalization supports a strong dividend yield. As investors will see throughout this article, the company’s impressive asset base and cash flow, even throughout a crash, make it a solid investment.

Simon Property Group – The Motley Fool

{kind=link}

Simon Property Group and Taubman

One of the major announcements to come out of Simon Property Group recently was the company announcing the end of its acquisition of Taubman Centers (NYSE: TCO.PK). The acquisition, originally priced at $3.6 billion, was to be paid entirely in cash. Since it was called off, Taubman Centers share price has collapsed, with its market capitalization now less than $2.3 billion.

Simon Property Group – IndyStar

Simon Property Group announced that calling off the merger would be based on two things. The first was the company argued that Taubman Centers hadn’t taken appropriate steps, as it was obligated too, in anticipating of COVID-19. Secondly, the company argued that it was allowed to leave the acquisition under the situation where COVID-19 disproportionately affected the company.

Given that Taubman Centers focuses on higher end malls in major cities supported by tourism, this point seems valid. The second point is more difficult to define. However, given that the market values Taubman Centers at roughly $2.3 billion, not counting the priced in belief that the merger could still happen, Simon Property Group clearly believes halting the merger will cost it <$1.3 billion.

Realistically, the company is probably right here. But even if it’s wrong, not only will it be able to delay the expenses from Taubman Centers through several years of lawsuits, it’ll be able to delay money owed for the acquisition by several years at least. Both of these things give the company a much stronger financial position through COVID-19.

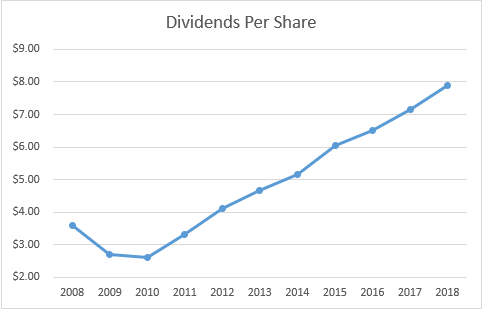

Simon Property Group 2008

Simon Property Group and its ability to generate future returns can be seen from how the company performed throughout the 2008 collapse in the markets.

<img src="https://static.seekingalpha.com/uploads/2020/7/6/saupload_DPS.png" alt="Simon Property Group (NYSE:SPG): A High Yield and High Risk REIT …” data-width=”483″ data-height=”309″ data-og-image-twitter_small_card=”true” data-og-image-twitter_large_card=”true” data-og-image-twitter_image_post=”true” data-og-image-msn=”true” data-og-image-facebook=”false” data-og-image-google_news=”true” data-og-image-google_plus=”true” data-og-image-linkdin=”true”>

Simon Property Group Dividends Per Share – Dividend Property Investor

{kind=link}

As a result of the 2008 collapse of the markets, one of the most significant collapses in the real estate markets, the company was forced to cut its dividend by almost 30%. That was a significant dividend cut that highlighted how the collapse affected even the best tier real estate companies. For Simon Property Group and COVID-19, the company has said it plans to cut its dividend by <50%.

In the 2008 real estate collapse, dividends that were cut in 2008 didn’t fully recover until 2012, although they had mostly recovered by 2011.

Simon Property Group announced for the second quarter it’d be cutting its dividends to $1.30 / share and that the company anticipates paying out $6 / share in 2020. Based on the company’s current market capitalization this indicates a near 9% yield for 2020, the worst year of the COVID-19 related crash. After this we expect a significant recovery.

Going back to the previous dividend, even if it takes a few years, would represent double-digit cash flow for investors who invest today.

Simon Property Group COVID-19

Simon Property Group has been forced to make a number of decisions as a result of COVID-19. However, the company has done an admirable job. On top of the discussion above of Taubman Centers, the company has taken strong steps to improve its liquidity and improve its customers.

Simon Property Group Credit Facility – Simon Property Group Press Release

Simon Property Group extended its credit facility from $4 billion recently to $6 billion with aggregate revolving commitments for up to $7 billion. The facilities mature from 2022-2024 and can be extended for a period of up to 1 year. Additionally, the company has managed to keep its interest rate at an incredibly low 70 basis points above LIBOR.

Given current LIBOR rates, the interest rate on the company’s credit facility is <1.5%. Given the multi-year time frame, Simon Property Group is incredibly well positioned with low cost money it can borrow to support itself.

Additionally, the company was forced to shutdown its malls recently, but it has recently reopened them. However, in the mean time the company has cut salaried employees paychecks by ~20% and has cut R&D investment by roughly $1 billion. These two things together provide the company with cost savings that will continue through the downturn and support the company.

However, what’s important to note here is that on top of significant cost savings, the company’s annual revenue is less than $6 billion. That means the company has low interest credit facilities to cover more than a year of fully lost revenue. This highlights the strength of the company’s financial positions in the markets. And it highlights the company’s ability to survive COVID-19.

While shareholders panic, bankers take careful assessment of the risk and realize, supported by the low interest rates they offer, the security of Simon Property Group.

Simon Property Group Risk

Longer term, the aspect of Simon Property Group to pay close attention to, and the risk is the purported decline of retail and the company’s move towards more luxurious properties, as shown by Taubman Centers acquisition.

Countless authors have discussed this risk, however, we choose to see it in a simple realistic light. The reality of the matter is that, at the end of the day, in certain market segments like clothes, groceries, etc., going to the store has tangible benefits. It’s also worth noting that many delivery services are hiding their true cost from consumers in the name of growth.

In a world where these two things are resolved, as mixed retail continues to grow, we expect malls to continue to play a smaller, but still significant part in people’s lives. Simon Property Group’s unparalleled financials make it, in our view, likely to play a significant roll in this. The company is, at a near double-digit yield, priced for minimal success.

That doesn’t mean that there’s no risk, but it does mean the risk-reward equation favors reward.

Conclusion

Simon Property Group is a significant investment, with significant potential. The company announced a dividend cut, but like management previously indicated it was less than 50%, and still gives investors a near 9% yield on cost. Investors overreacted to COVID-19, even around news articles of a second wave, as the market gradually begins to reopen.

Simon Property Group’s significant financial strength and attempts to end the Taubman Centers acquisition support it through the current crisis. After that, in a normalized investment world, the company is significantly undervalued. That makes it an exciting opportunity, one that we recommend investors pay close attention to for the long run.

The Energy Forum can help you build and generate high-yield income from a portfolio of quality energy companies. Worldwide energy demand is growing quickly, and you can be a part of this exciting trend.

The Energy Forum provides:

- Managed model portfolio to generate you high-yield returns.

- Deep-dive research reports about quality investment opportunities.

- Macroeconomic overviews of the oil market.

- Technical buy and sell alerts.

Disclosure: I am/we are long SPG. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

|

|

Leave a Reply

You must be logged in to post a comment.